Why the Strait of Hormuz Matters: Geography, Oil, and Global Power

A narrow strip of water — barely 33 kilometres wide at its tightest point — holds the global economy in its grip. The Strait of Hormuz, wedged between Iran to the north and Oman and the UAE to the south, is the single most important oil shipping route on Earth. No other waterway comes close to matching its strategic weight.

Every day, roughly 20 million barrels of oil and oil products pass through this corridor. That figure, drawn from US Energy Information Administration estimates for 2025, represents nearly one in every five barrels of oil consumed globally. Moreover, approximately 20% of the world’s liquefied natural gas — most of it originating from Qatar — travels the same path. In annual terms, that amounts to nearly $600 billion worth of energy trade. Consequently, what happens in this narrow channel affects fuel prices, electricity bills, and food costs in countries thousands of miles away.

The strait’s importance, however, extends far beyond oil. It is also a critical route for fertiliser exports, food imports, medicines, and technological supplies serving the wider Middle East. In short, the Strait of Hormuz is not merely an energy chokepoint. It is a lifeline for modern civilisation’s most essential supply chains.

Yet for all its economic significance, the strait sits in one of the world’s most politically volatile regions. Iran controls the northern coastline and, under international maritime law, its territorial waters extend across the strait’s narrowest shipping lanes. As a result, Iran holds an extraordinary degree of leverage over the global economy — leverage it has threatened to use, and in 2025, effectively deployed.

When Iran moved to block the strait following US and Israeli military strikes in February 2025, the consequences were immediate and severe. Global fuel prices surged. Shipping traffic collapsed by around 95%. Fuel rationing appeared in Europe. Governments across Asia cut working weeks and closed universities to conserve energy supplies. The disruption demonstrated, with striking clarity, why this 33-kilometre stretch of water commands the attention of every major power on Earth.

This article explains everything you need to know. It covers the strait’s geography, its extraordinary economic role, the legal questions surrounding who actually controls it, the full history of threats to its security, and the limited options the world has for working around it. Whether you are trying to understand the 2025 Iran conflict, the mechanics of global oil markets, or the long-term vulnerabilities of the world’s energy supply chains, the Strait of Hormuz is where that story begins.

Table of Contents

Strait of Hormuz Explained - Video Guide

What Is the Strait of Hormuz? Geography and Strategic Position

📌 Key Facts at a Glance

- Location: Between Iran (north) and Oman/UAE (south), connecting the Persian Gulf to the Arabian Sea

- Width at narrowest point: Approximately 33km (21 miles)

- Daily oil flow: ~20 million barrels (2025, US EIA)

- Annual energy trade value: Nearly $600 billion

- Share of global oil supply: ~20%

- Share of global LNG supply: ~20%

- Countries most exposed: China, India, Japan, South Korea, and much of Europe

The Strait of Hormuz is a narrow maritime corridor connecting the Persian Gulf to the Gulf of Oman and, beyond that, to the Arabian Sea and the wider Indian Ocean. It sits at the southeastern tip of the Persian Gulf, bounded to the north by Iran and to the south by the Sultanate of Oman and the United Arab Emirates. On a world map, it appears almost unremarkable — a small pinch point between two landmasses. In geopolitical and economic reality, however, it is arguably the most consequential stretch of water on the planet.

Where Exactly Is the Strait of Hormuz Located?

Geographically, the strait lies between approximately 26° and 27° north latitude, placing it squarely within the broader Middle East region. To its west lies the Persian Gulf, a semi-enclosed body of water bordered by Iran, Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar, and the UAE. To its east lies the Gulf of Oman, which opens into the Arabian Sea and ultimately connects to the Indian Ocean’s global shipping network.

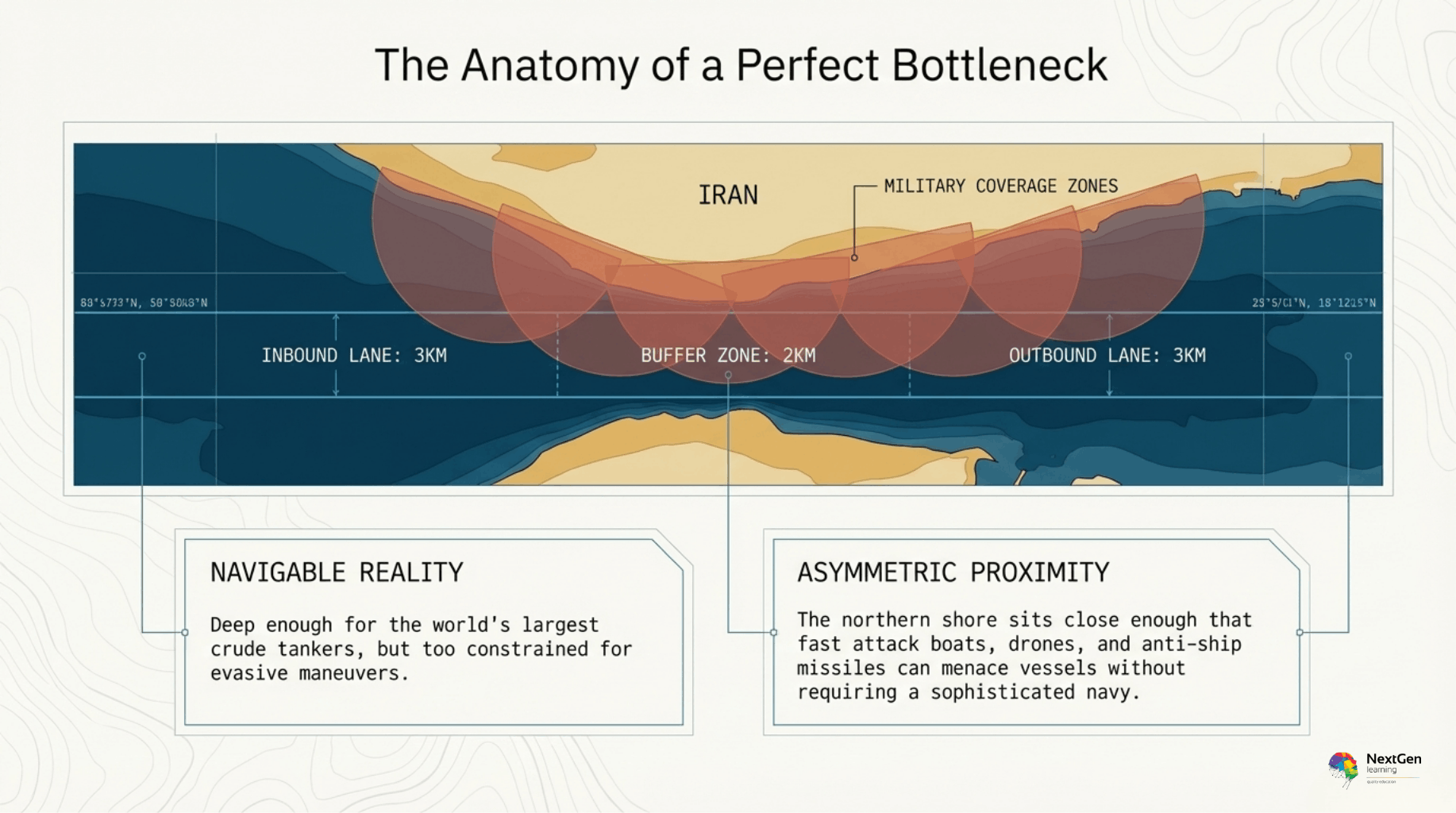

The strait is not a single open channel. Instead, it operates through two designated shipping lanes — one for inbound vessels and one for outbound — each roughly three kilometres wide. These lanes are separated by a two-kilometre buffer zone. Consequently, the actual navigable corridors that global oil tankers use are remarkably narrow. Furthermore, at the strait’s tightest point, both shipping lanes fall entirely within the territorial waters of Iran and Oman. This geographical reality has profound legal and strategic implications, which we explore in detail later in this article.

The nearest major cities to the strait include Bandar Abbas in Iran — the country’s most important commercial port — and Muscat, the capital of Oman. The UAE port of Fujairah sits just outside the strait on the Gulf of Oman side, which is precisely why it has become strategically significant as an alternative oil export hub.

How Wide Is the Strait of Hormuz — and Why Does That Matter?

At its entrance and exit, the strait measures approximately 50 kilometres (31 miles) across. However, at its narrowest navigable point, the width shrinks to roughly 33 kilometres (21 miles). To put that in perspective, this is narrower than the English Channel at its tightest point, and far narrower than most major international shipping routes.

That narrowness is precisely what makes Hormuz so strategically dangerous. A wide ocean passage is extraordinarily difficult to threaten or block. A narrow channel, by contrast, can be monitored, mined, or menaced by a relatively small military force operating from the adjacent coastline. Iran’s northern shore sits close enough to the shipping lanes that shore-based missiles, drones, and fast attack boats can all pose credible threats to passing vessels — without Iran needing to deploy a large or sophisticated navy.

Moreover, the strait is deep enough to accommodate the world’s largest crude oil tankers, known as Very Large Crude Carriers (VLCCs) and Ultra Large Crude Carriers (ULCCs). These vessels can carry up to 3 million barrels of oil in a single journey. Their sheer size means they cannot simply take alternative routes — most other potential bypass waterways are too shallow, too distant, or too commercially impractical for regular use at scale.

Why the Strait Has No Practical Replacement

This combination of factors — narrow width, legal complexity, deep water accommodating massive tankers, and the absence of viable alternatives — is what elevates Hormuz from a regional waterway to a global strategic asset. Energy analysts frequently describe it as the world’s single most important oil chokepoint, a designation we examine in detail in the next section.

Importantly, the strait’s geography has remained constant throughout history. What has changed is the volume of trade passing through it and the military capabilities of the states that border it. As global energy demand grew throughout the 20th century, and as Middle Eastern oil production expanded to meet it, the Strait of Hormuz steadily became more and more indispensable. Today, there is simply no realistic substitute. As a result, every major oil-importing nation — from China and India to Japan, South Korea, and the countries of Western Europe — has a direct and vital interest in keeping this narrow channel open.

{kind=link}

{kind=link}

How Much Oil and Gas Passes Through the Strait of Hormuz?

To understand why the Strait of Hormuz commands such intense global attention, it helps to look closely at the sheer scale of what moves through it every single day. The numbers are staggering — and they touch virtually every corner of the world economy.

Oil Volumes and Annual Trade Value

According to estimates from the US Energy Information Administration, approximately 20 million barrels of oil and oil products passed through the Strait of Hormuz per day in 2025. That figure represents close to 20% of total global oil consumption. In other words, roughly one in every five barrels of oil used anywhere in the world — to fuel vehicles, generate electricity, heat homes, and power industry — travels through this single narrow corridor.

In annual terms, that volume translates to nearly $600 billion worth of energy trade. To place that figure in context, it exceeds the entire GDP of many mid-sized economies. Consequently, even a partial disruption to traffic through the strait sends immediate and measurable shockwaves through global energy markets. When Iran effectively blocked the waterway in early 2025, oil prices surged almost instantly. Conversely, when the ceasefire was announced and safe passage was guaranteed, prices dropped by around 15% within hours — a powerful illustration of just how directly Hormuz influences the global price of energy.

The oil flowing through the strait does not come from Iran alone. In fact, the majority originates from other Gulf states, including:

- Saudi Arabia — the world’s largest oil exporter and the single biggest contributor to Hormuz traffic

- Iraq — heavily dependent on the strait for virtually all of its oil export revenues

- Kuwait — with limited pipeline infrastructure, Kuwait relies almost entirely on Hormuz for its exports

- Qatar — a major oil producer in addition to its dominant role in LNG exports

- The UAE — a significant oil exporter, though it has developed some bypass capacity

This means that even if Iran were somehow excluded from the equation entirely, the strait would remain critical. Blocking Hormuz does not just hurt Iran’s economy — it simultaneously damages the economies of Iran’s regional rivals and customers across the globe. That paradox is central to understanding the strait’s geopolitical complexity.

LNG Exports Through Hormuz — Qatar’s Critical Role

Beyond crude oil, the Strait of Hormuz is the world’s most important corridor for liquefied natural gas. Approximately 20% of global LNG supply passes through the strait, and Qatar accounts for the overwhelming majority of that volume.

In 2024, Qatar exported approximately 9.3 billion cubic feet per day of LNG through the strait. The UAE contributed an additional 0.7 billion cubic feet per day. Together, these two nations make the Strait of Hormuz irreplaceable for global gas markets — not just oil markets.

It is worth briefly explaining what LNG actually is, because its significance is often underappreciated. Liquefied natural gas is natural gas that has been cooled to around -162°C, at which point it becomes liquid and occupies approximately 600 times less space than in its gaseous state. This dramatic reduction in volume makes it practical to transport by sea in specialised tanker ships. Upon arrival at its destination, the LNG is warmed and converted back into gas, where it is then used for heating, cooking, electricity generation, and industrial processes.

For countries in Asia and Europe that cannot access natural gas via pipeline — and that number is large — LNG shipped through the Strait of Hormuz is not a luxury. It is essential infrastructure. Japan, for instance, generates a significant portion of its electricity from gas-fired power plants and imports virtually all of its LNG by sea. South Korea faces a similar dependency. Therefore, any disruption to Hormuz does not merely raise fuel prices — it threatens the basic energy security of entire nations.

Beyond Oil and Gas — Fertiliser, Food, and Medicines

The strategic significance of the Strait of Hormuz extends well beyond hydrocarbons. This is a dimension that receives far too little attention in most analyses of the waterway.

Approximately one-third of the world’s fertiliser trade normally passes through the strait. This is a direct consequence of the Middle East’s dominance in natural gas production, since natural gas is the primary feedstock used to manufacture nitrogen-based fertilisers. Countries such as Qatar, Saudi Arabia, and Iran are among the world’s largest fertiliser exporters, and virtually all of their output reaches global markets via the Strait of Hormuz.

The implications of this are profound. Fertiliser is not a luxury commodity — it is the foundation of modern agricultural production. A sustained disruption to fertiliser supplies through Hormuz would, over time, reduce crop yields, raise food prices, and threaten food security in developing nations that depend on affordable imports. In this way, the strait’s closure creates a ripple effect that extends far beyond the energy sector.

Moreover, the strait serves as a vital import corridor for the Middle East itself. The region relies heavily on seaborne imports of:

- Food and agricultural products — particularly grains, which Gulf states import in large quantities

- Medicines and medical equipment — critical for healthcare systems across the region

- Consumer goods and technology — from electronics to industrial machinery

- Construction materials — supporting the Gulf’s ongoing infrastructure development

Consequently, closing the Strait of Hormuz does not only damage oil-exporting nations’ revenues. It simultaneously cuts off the very imports those nations need to sustain their populations and economies. This two-way dependency makes any prolonged blockade economically self-destructive for all parties involved — including Iran itself.

The Scale of Daily Shipping Traffic

Under normal conditions, approximately 3,000 ships transit the Strait of Hormuz every month. That works out to roughly 100 vessels per day — a continuous procession of supertankers, LNG carriers, container ships, bulk carriers, and other commercial vessels moving in both directions through the designated shipping lanes.

During the 2025 Iran conflict, that figure collapsed dramatically. BBC Verify analysis showed that daily traffic fell by approximately 95% compared to pre-conflict levels. The combination of Iranian military threats, drone and missile attacks on vessels, and the near-impossibility of obtaining affordable insurance for ships attempting to transit the strait effectively brought one of the world’s busiest waterways to a near-standstill.

That near-standstill, sustained over a period of weeks, was enough to trigger fuel rationing in Europe, government-mandated energy conservation measures across Asia, and electricity restrictions in parts of Africa. It demonstrated, in the starkest possible terms, just how much of the world’s daily functioning depends on the uninterrupted flow of traffic through a corridor barely 33 kilometres wide.

If you’re interested in how global oil flows, pricing, and energy security work in real-world scenarios, explore our Oil and Gas Management course to gain deeper insight into this critical industry.

Why Is the Strait of Hormuz Called the World's Most Important Oil Chokepoint?

The term “chokepoint” is used frequently in discussions of global energy security, but its full meaning is rarely explained. Understanding what a chokepoint actually is — and why Hormuz sits at the very top of the hierarchy — is essential for grasping the strait’s true strategic weight.

What Is an Oil Chokepoint?

A maritime chokepoint is a narrow navigational passage through which a disproportionately large volume of global trade must flow. The defining characteristic of a chokepoint is not simply that it is narrow. Rather, it is that the combination of narrowness, high traffic volume, and the absence of practical alternatives makes it uniquely vulnerable to disruption. If traffic is blocked, rerouted, or threatened at a chokepoint, the consequences ripple outward across global supply chains with speed and severity that would be impossible if the same trade moved through open ocean.

The world has several recognised maritime chokepoints. Each carries significant strategic weight. However, they are not equal in importance. The volume of energy trade they carry, the feasibility of alternative routes, and the geopolitical instability of their surrounding regions vary considerably. Consequently, energy analysts and defence strategists rank them in terms of global risk, and the Strait of Hormuz consistently sits at the top of that ranking.

How Hormuz Compares to Other Global Chokepoints

To appreciate Hormuz’s singular importance, it is worth comparing it directly to the world’s other major maritime chokepoints.

The Suez Canal — Egypt The Suez Canal connects the Red Sea to the Mediterranean, providing a critical shortcut between Asian and European markets. It handles a significant portion of global container trade and some oil shipments. However, unlike Hormuz, the Suez Canal has a meaningful bypass alternative — the Cape of Good Hope route around southern Africa. This adds roughly two weeks of sailing time and increases costs substantially, but it is physically and commercially feasible for most vessel types. Moreover, the Suez Canal carries a far smaller share of global oil than Hormuz. When the Ever Given container ship blocked the canal for six days in March 2021, global trade was disrupted — but global oil markets were not fundamentally threatened.

The Strait of Malacca — Southeast Asia The Strait of Malacca, running between Malaysia, Singapore, and Indonesia, is the primary route connecting the Indian Ocean to the Pacific. It carries an enormous volume of trade, including significant quantities of oil destined for China, Japan, and South Korea. However, alternative routes through the Lombok Strait and the Sunda Strait in Indonesia exist, albeit at greater distance and cost. Furthermore, the Strait of Malacca is bordered by stable, commercially oriented nations with strong incentives to keep it open. The geopolitical risk profile is therefore considerably lower than that of Hormuz.

Bab el-Mandeb — Yemen/Djibouti The Bab el-Mandeb Strait connects the Red Sea to the Gulf of Aden and lies at the southern entrance to the Suez Canal route. It is highly strategically significant, and Houthi attacks on shipping in this area from 2023 onwards demonstrated its vulnerability. However, oil that cannot pass through Bab el-Mandeb can still reach global markets via alternative routes. The same cannot be said for oil that cannot exit the Persian Gulf through Hormuz.

The Turkish Straits — Bosphorus and Dardanelles These narrow waterways connect the Black Sea to the Mediterranean and carry Russian and Caspian oil exports. They are geopolitically sensitive, particularly given Russia’s role in European energy supply. However, in terms of sheer volume of oil trade, they carry significantly less than Hormuz.

The comparison table below illustrates the key differences clearly:

Chokepoint | Daily Oil Flow | Viable Bypass? | Geopolitical Risk | Global Ranking |

Strait of Hormuz | ~20 million barrels | Very limited | Extremely high | #1 |

Strait of Malacca | ~16 million barrels | Partial | Moderate | #2 |

Suez Canal | ~5 million barrels | Yes (Cape route) | Moderate | #3 |

Bab el-Mandeb | ~6 million barrels | Partial | High | #4 |

Turkish Straits | ~3 million barrels | Very limited | Moderate-High | #5 |

Sources: US Energy Information Administration; US Naval Institute; International Energy Agency estimates.

Why Hormuz Has No Equal

What elevates Hormuz decisively above all other chokepoints is the convergence of three factors that do not exist in combination anywhere else in the world.

First, the volume of oil and gas it carries is simply unmatched. No other single waterway comes close to handling 20% of global oil supply and 20% of global LNG simultaneously. Disrupting Hormuz therefore strikes at both the liquid fuels that power transport and industry, and the gas that heats homes and generates electricity across Asia and Europe.

Second, the bypass alternatives are genuinely inadequate. As we explore in detail later in this article, the existing pipeline infrastructure that bypasses Hormuz can handle only a fraction of normal traffic. Even operating at full capacity, bypass routes would leave a shortfall of 8 to 10 million barrels per day — a gap so large it would represent the most severe supply shock in the history of global oil markets.

Third, the geopolitical environment surrounding Hormuz is uniquely volatile. Unlike the Strait of Malacca — bordered by stable, trade-dependent nations — Hormuz sits between Iran and its neighbours at a moment of profound regional tension. Iran has both the motivation and the military capability to threaten traffic through the strait. Furthermore, because Iran’s northern coastline extends along the entire length of the strait, it enjoys a geographical advantage that no other nation holds at any other major chokepoint.

The Chokepoint Paradox

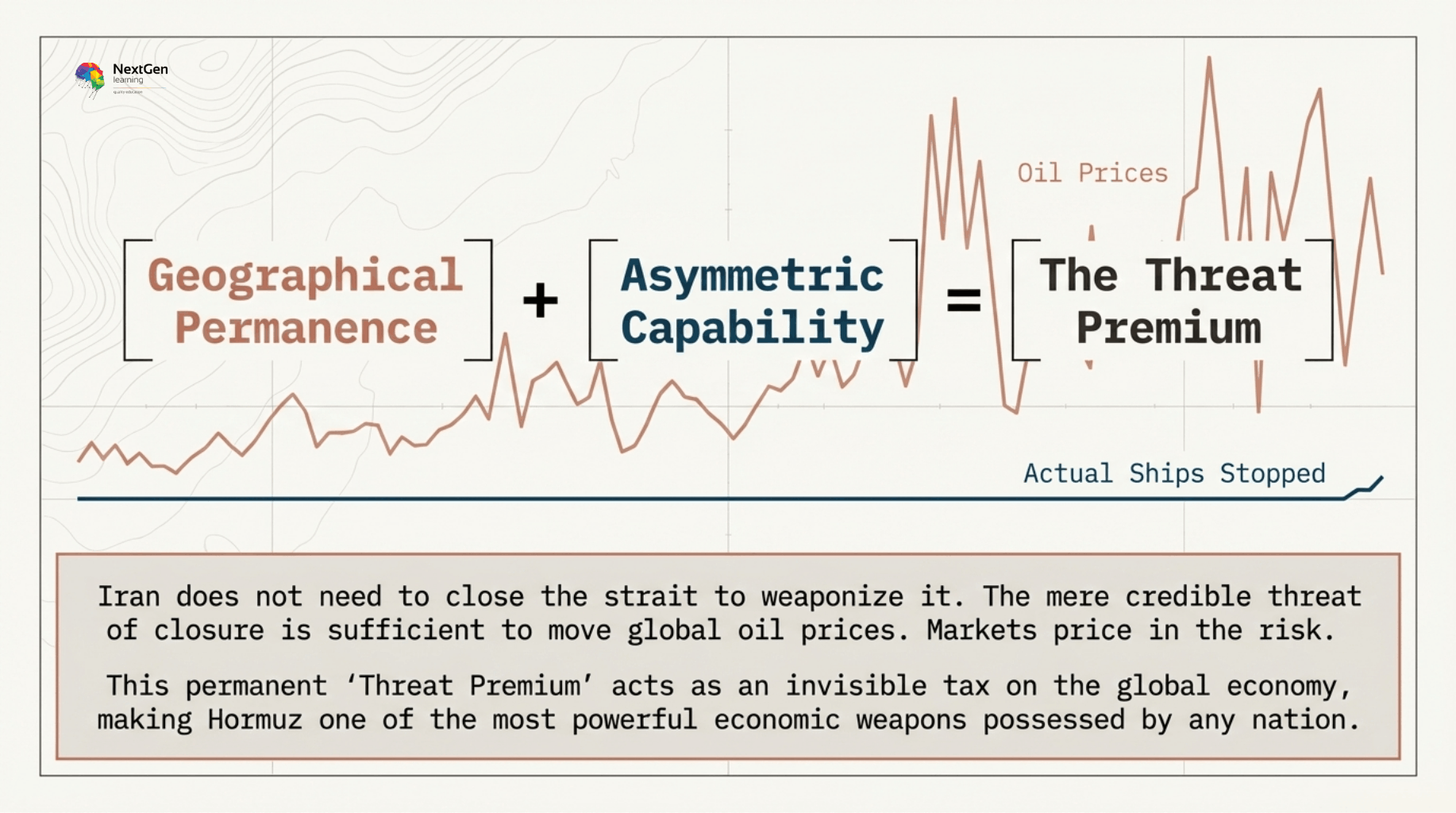

There is a deeper paradox at the heart of Hormuz’s strategic importance. The strait is so critical that even the threat of closure — without any actual blockade — is enough to move global oil prices significantly. Markets price in risk. Consequently, whenever tensions rise in the Persian Gulf, energy traders around the world adjust their positions, insurers raise their premiums, and fuel costs rise for consumers everywhere — regardless of whether a single tanker has actually been stopped.

This means Iran does not need to close the strait entirely to extract geopolitical leverage from it. The mere credible threat of closure is itself a powerful instrument of economic pressure. It is, in the language of strategic studies, a form of deterrence — and it is a form of deterrence that no other nation on Earth currently possesses in quite the same way. Understanding this dynamic is essential for understanding not just the Strait of Hormuz, but the entire strategic logic of Iran’s regional posture.

Understanding how uncertainty affects markets is a key professional skill — the Risk Management course teaches how to analyse and respond to complex global risks.

Who Controls the Strait of Hormuz — and What Does International Law Say?

One of the most frequently misunderstood aspects of the Strait of Hormuz is the question of control. Many people assume that because the strait is an international waterway, no single nation can legally close it. The reality, however, is considerably more nuanced — and considerably more unsettling for the countries that depend on it.

Iran’s Territorial Waters and Legal Control

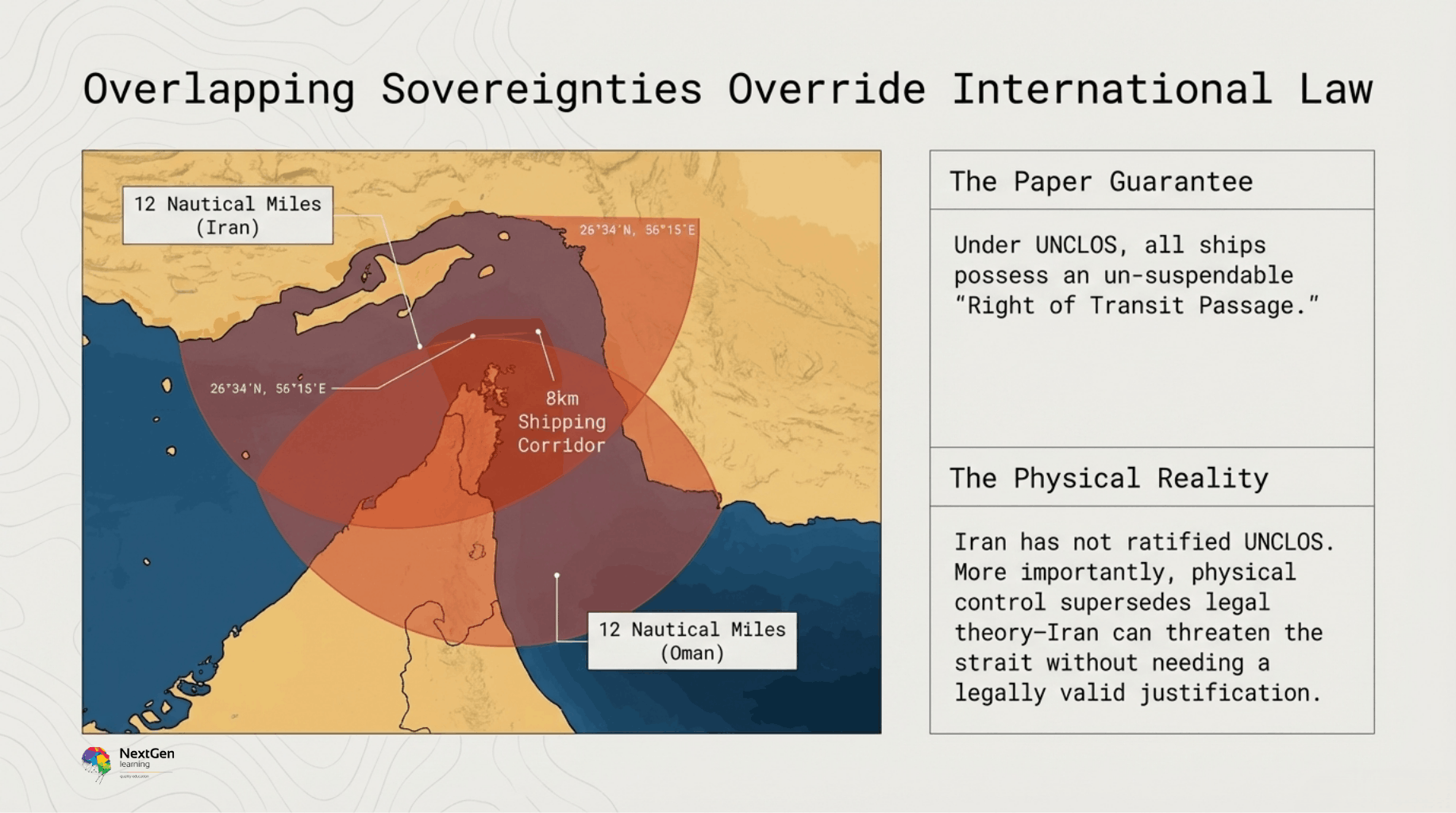

Under international maritime law, coastal nations exercise sovereignty over their territorial seas. The United Nations Convention on the Law of the Sea, commonly known as UNCLOS, defines territorial waters as extending up to 12 nautical miles — approximately 22 kilometres — from a nation’s coastline. Within this zone, a coastal state has full sovereignty, subject to certain internationally recognised exceptions.

This legal framework has enormous practical consequences for the Strait of Hormuz. At its narrowest point, the strait measures approximately 33 kilometres across. Iran’s territorial waters extend 12 nautical miles from its northern coastline. Oman’s territorial waters extend 12 nautical miles from its southern coastline. Together, these two zones cover the entire width of the strait at its narrowest point — including both designated shipping lanes.

In other words, there is no section of the strait’s critical navigable passage that falls in international waters. Every ship transiting the Strait of Hormuz is, at some point, passing through either Iranian or Omani territorial waters. This geographical and legal reality gives Iran a degree of formal jurisdiction over the waterway that most people — including many policymakers — do not fully appreciate.

The Right of Innocent Passage Under UNCLOS

However, Iran’s territorial sovereignty over its portion of the strait does not give it an unlimited right to block all traffic. UNCLOS enshrines two important legal principles that constrain what coastal states can do in straits used for international navigation.

The first is the right of innocent passage. Under UNCLOS, all ships — regardless of flag or nationality — have the right to pass through territorial waters continuously and expeditiously, provided their passage is not prejudicial to the peace, good order, or security of the coastal state. Innocent passage applies in territorial seas generally and provides a baseline level of access to foreign vessels.

The second, and more powerful, principle is the right of transit passage. This applies specifically to straits used for international navigation between one area of high seas and another — which describes the Strait of Hormuz precisely. Under transit passage rules, all ships and aircraft enjoy the right of continuous and expeditious transit through international straits. Crucially, coastal states cannot suspend this right, even temporarily. Furthermore, coastal states cannot impose conditions on transit passage that would effectively deny, hamper, or impair it.

On paper, therefore, Iran cannot legally close the Strait of Hormuz under UNCLOS. The right of transit passage is specifically designed to prevent exactly this kind of unilateral closure of internationally critical waterways.

Why Iran Can — and Cannot — Fully Close the Strait Legally

The legal picture, however, is complicated by two important realities.

First, Iran has never ratified UNCLOS. Tehran signed the convention but did not ratify it, and has historically argued that it is not bound by all of its provisions. Iran instead asserts a more expansive interpretation of its rights over its territorial waters — one that gives it greater discretion to regulate or restrict passage. Most international legal scholars reject Iran’s position, but international law without enforcement is, in practice, aspirational rather than binding.

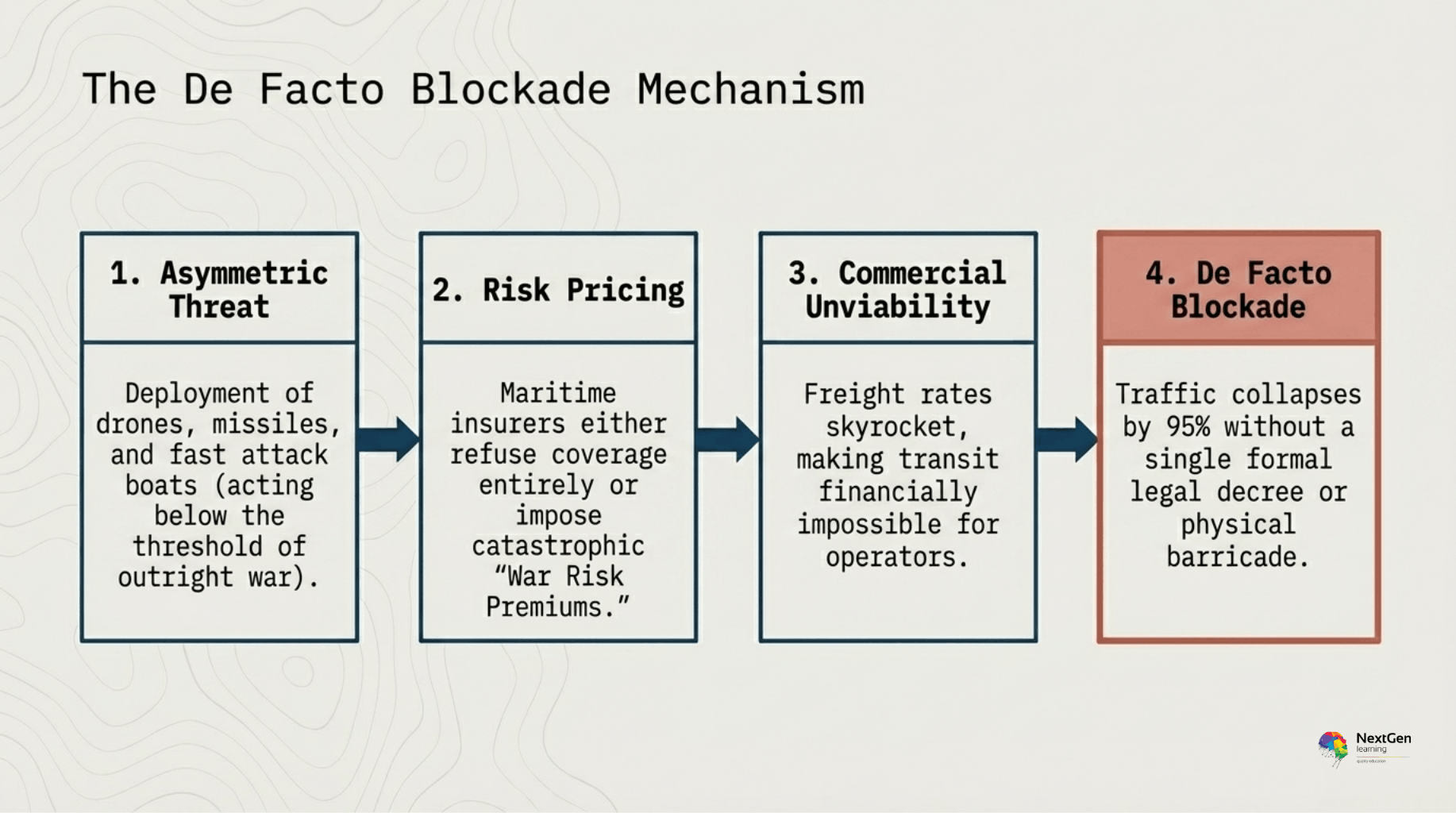

Second, and more practically, the distinction between legal rights and physical capabilities matters enormously. Iran does not need a legally valid justification to threaten ships in the strait. It simply needs the military means to make passage dangerous enough that commercial operators choose not to attempt it. During the 2025 conflict, Iran achieved precisely this outcome. It did not formally declare the strait closed. Instead, it deployed drones, missiles, fast attack boats, and potentially sea mines to create conditions under which insurers refused to cover vessels, ship operators refused to send their crews into harm’s way, and traffic collapsed by approximately 95% without a single formal legal decree.

This is an important strategic lesson. Iran’s power over the Strait of Hormuz is not primarily legal — it is physical and psychological. The threat of attack, combined with the collapse of commercial insurance coverage, is sufficient to achieve a de facto blockade even when a de jure one would be internationally unlawful.

Oman’s Role — The Overlooked Factor

While Iran dominates discussions of Hormuz control, Oman’s role deserves more attention than it typically receives. Oman controls the southern coastline of the strait and, like Iran, has territorial waters that extend across part of the navigable passage. However, Oman has consistently maintained a policy of neutrality and open access. It has strong diplomatic and economic incentives to keep the strait open — its own trade and energy exports depend on it — and it has historically served as an informal back-channel between Iran and Western nations during periods of tension.

Oman’s cooperative stance means that, in practice, Iran is the only coastal state with both the motivation and the military capability to threaten transit through Hormuz. Nevertheless, Oman’s legal position is a reminder that the strait’s governance involves more than one nation, and that diplomatic engagement with Muscat remains a valuable tool for international efforts to maintain freedom of navigation.

The United States and Freedom of Navigation

The United States has long maintained that freedom of navigation in international straits is a core principle of the international order — one it is prepared to defend militarily. The US Navy has historically conducted Freedom of Navigation Operations in contested waters around the world, precisely to resist legal claims by coastal states that would restrict international access.

In the context of Hormuz, the US position has been consistent: transit passage is a right, not a privilege, and no nation can lawfully suspend it. However, as the 2025 conflict demonstrated, asserting that legal position and enforcing it in practice are two very different things. The US confined its military response largely to air strikes on Iranian military infrastructure, including anti-ship missile sites along the strait, rather than deploying warships directly into the contested waterway. This reflected the genuine difficulty of guaranteeing safe passage through a narrow channel against a determined coastal defender armed with modern anti-ship weapons.

Consequently, the legal framework governing the Strait of Hormuz is best understood not as a reliable guarantee of open access, but as a normative standard that shapes international expectations and diplomatic pressure — while falling well short of providing physical security on its own. The real guarantor of open passage through Hormuz is not international law. It is the balance of military power, economic incentives, and diplomatic engagement among the nations with the most at stake.

These tensions reflect the importance of diplomacy and negotiation — the Conflict Resolution and Mediation in International Relations course explores how global conflicts are managed and resolved.

What Happens When the Strait of Hormuz Is Blocked?

The closure of the Strait of Hormuz is not a theoretical scenario confined to academic risk assessments and military planning documents. The 2025 Iran conflict demonstrated, with painful clarity, what actually happens when traffic through the world’s most important oil chokepoint is severely disrupted. The consequences were immediate, cascading, and genuinely global — affecting not just energy markets but daily life for hundreds of millions of people across multiple continents.

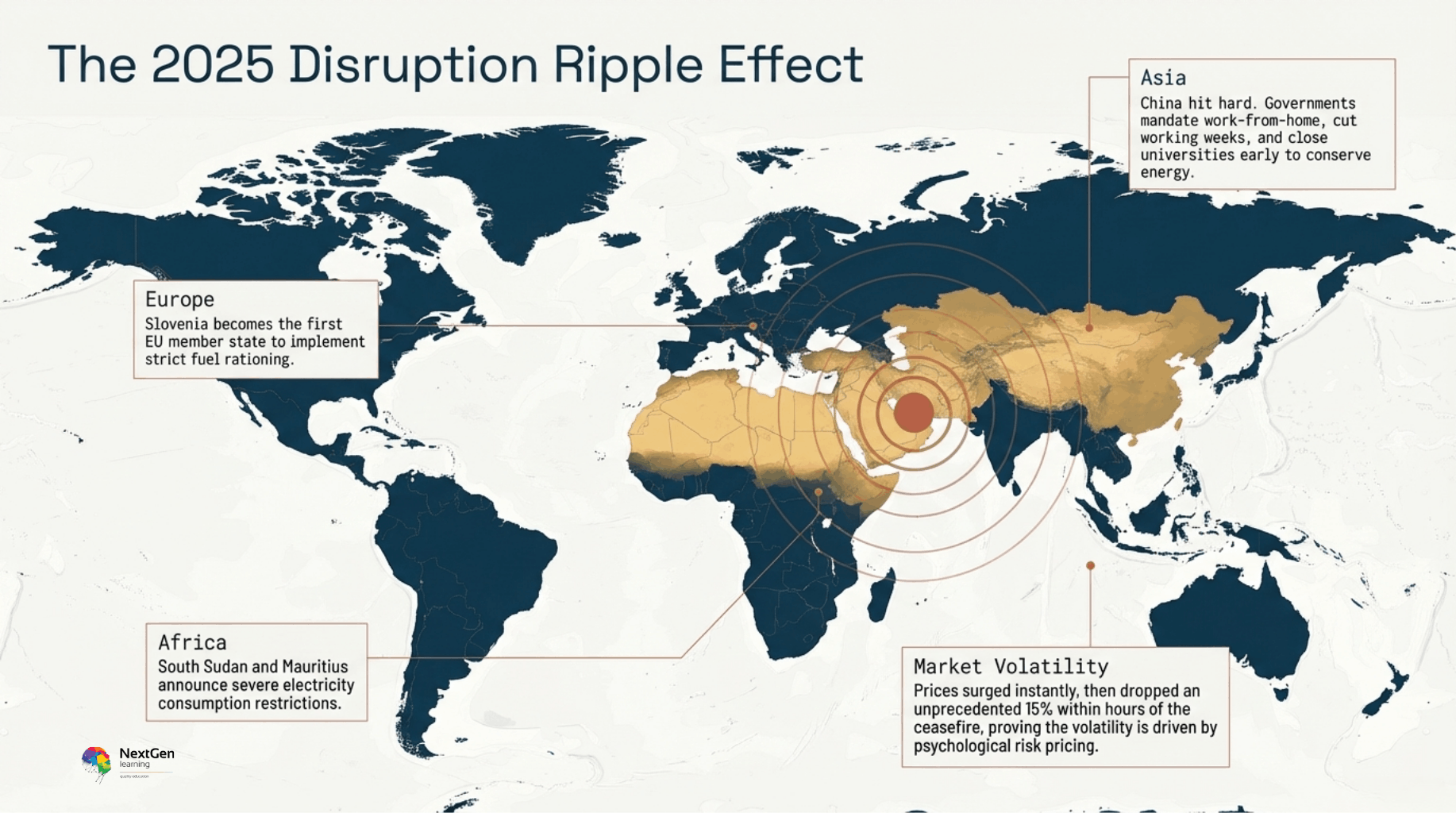

- Energy markets: Oil prices surged immediately, then dropped 15% within hours of the ceasefire announcement

- Asia: Governments cut working weeks, closed universities, and ordered work-from-home measures to conserve supply

- Europe: Slovenia became the first EU member state to implement fuel rationing since the 1970s

- Africa: South Sudan and Mauritius imposed electricity consumption restrictions

- Shipping: Insurance coverage collapsed, freight rates surged, and 95% of commercial traffic stopped

Impact on Global Oil Prices

The most immediate and visible consequence of a Hormuz disruption is a sharp spike in global oil prices. Energy markets are extraordinarily sensitive to supply signals, and the Strait of Hormuz is the single largest supply variable in the global oil equation. When credible threats to the strait emerge, traders begin pricing in the risk of reduced supply before a single barrel is actually lost. Consequently, price movements can precede physical disruption by days or even weeks.

During the 2025 conflict, global fuel prices soared as Iran’s blockade took effect. The speed and severity of the price response reflected not just the actual reduction in supply, but the market’s uncertainty about how long the disruption would last and how severe it would become. This uncertainty premium — the additional cost that markets attach to unpredictable supply risk — is itself a significant economic burden. It raises costs for airlines, shipping companies, manufacturers, and ultimately consumers, even in countries that do not directly import Gulf oil.

When the ceasefire was announced and safe passage through the strait was guaranteed, oil prices dropped by approximately 15% within hours. That single data point illustrates the extraordinary leverage that Hormuz holds over global energy pricing. No other single event — no OPEC production decision, no US shale output change, no demand shift from China — routinely moves global oil prices by 15% in a matter of hours.

The longer a Hormuz disruption persists, the more severe and difficult to reverse its price effects become. Strategic petroleum reserves, which governments maintain precisely for supply emergencies, can cushion short-term shocks. However, they are finite. The International Energy Agency estimates that collective IEA member reserves could cover roughly 50 days of net imports under normal circumstances. A prolonged Hormuz closure would exhaust those reserves and leave markets exposed to sustained price escalation with no immediate remedy.

Impact on Asia — China, India, Japan, and South Korea

No region of the world is more exposed to a Strait of Hormuz disruption than Asia. The continent’s major economies are simultaneously the world’s largest energy consumers and among the most dependent on Gulf oil and LNG imports. For them, Hormuz is not an abstraction — it is a daily operational necessity.

China is the world’s largest oil importer and purchases approximately 90% of the oil that Iran exports to the global market. However, China’s exposure to Hormuz extends well beyond Iranian oil. A substantial proportion of its total oil imports — from Saudi Arabia, Iraq, Kuwait, and the UAE — also transits the strait. Therefore, a Hormuz blockade strikes at the heart of China’s energy security regardless of the status of its relationship with Iran.

During the 2025 disruption, the impact on Chinese daily life was tangible and documented. The fuel crisis prompted governments across Asia to order employees to work from home, cut the working week, declare national holidays, and close universities early — all in an effort to conserve energy supplies. These measures reflected the genuine severity of the supply shock and the limited short-term options available to governments facing an acute energy emergency.

Japan and South Korea face perhaps the most acute vulnerability of any major economies. Both nations are almost entirely dependent on imported energy. Japan generates a large share of its electricity from gas-fired power plants following the post-Fukushima reduction in nuclear capacity, and imports virtually all of its LNG by sea from Gulf producers. South Korea similarly relies heavily on imported oil and gas for both electricity generation and industrial production. For both countries, a prolonged Hormuz closure is not merely an economic problem — it is an existential threat to national energy security.

India, meanwhile, sits in a strategically ambiguous position. It is one of the world’s fastest-growing energy consumers and imports a significant share of its oil from Gulf producers. However, India also has historically maintained diplomatic relationships with both Iran and the Western powers, giving it some room to navigate geopolitical disruptions. Nevertheless, a sustained Hormuz closure would inevitably drive up India’s import costs and strain its current account balance significantly.

Impact on Europe and the Wider Global Economy

Europe’s direct exposure to Hormuz is somewhat lower than Asia’s, primarily because European nations source a greater proportion of their energy from North Sea production, Norwegian gas, American LNG, and — historically — Russian pipeline gas. However, the indirect effects of a Hormuz disruption are still severe and far-reaching.

When Gulf oil cannot reach Asian markets via Hormuz, Asian buyers compete more aggressively for alternative supplies from other producing regions — including sources that Europe also relies upon. This increased competition drives up prices globally, regardless of where the oil originates. Consequently, European consumers and industries face higher energy costs even when their own supply chains are not directly disrupted.

The 2025 conflict provided a concrete illustration of this dynamic. Slovenia became the first EU member state to implement formal fuel rationing — a measure not seen in Europe since the 1970s oil crisis. This occurred not because Slovenia directly imports significant volumes of Gulf oil, but because the global price shock and supply uncertainty created by the Hormuz disruption made fuel sufficiently scarce and expensive to justify emergency rationing measures.

In Africa, the disruption’s impact was similarly significant. South Sudan and Mauritius both announced measures restricting electricity consumption — a stark reminder that the consequences of Hormuz disruptions are not confined to wealthy, energy-intensive economies. Developing nations, which typically have fewer energy diversification options and smaller fiscal buffers, are often among the most severely affected when global energy prices spike sharply.

Global disruptions like this highlight the importance of resilient logistics systems — our Supply Chain Management, Purchasing & Procurement course explains how businesses manage risks across international trade routes

Shipping Insurance and Freight Rate Surges

One dimension of a Hormuz disruption that receives insufficient attention is its impact on the shipping insurance market. This is, however, one of the most immediate and practically significant consequences for global trade.

The global shipping insurance market operates on the principle of assessed risk. When a waterway becomes a war zone — or even a credible threat environment — insurers respond by either refusing to cover vessels transiting that route, or by imposing war risk premiums so severe that the economic case for transit collapses. During the 2025 conflict, this is precisely what happened in the Strait of Hormuz.

As Arne Lohmann Rasmussen, chief analyst at Global Risk Management, explained during the crisis, ships attempting to transit the strait faced the prospect of attack with either no insurance coverage available or premiums so prohibitively expensive that operators could not justify the risk. For commercial shipping companies, operating without adequate insurance is not simply inadvisable — it is typically prohibited by their financing arrangements and regulatory obligations. Therefore, even ships whose captains might have been willing to attempt the passage were prevented from doing so by the collapse of the insurance market.

Freight rates — the cost of chartering a vessel to move cargo — surged in response to the reduced supply of ships willing to operate in the region. Higher freight rates, in turn, feed directly into the cost of goods, further amplifying the inflationary impact of the disruption across global supply chains.

This insurance and freight rate dynamic explains why a Hormuz disruption can effectively shut down maritime traffic even without Iran physically stopping every ship that attempts to pass. The combination of credible military threat and insurance market collapse creates a self-reinforcing cycle in which commercial operators voluntarily withdraw from the route — achieving Iran’s strategic objective without requiring a sustained military campaign to enforce it.

The Fertiliser and Food Security Dimension

As noted earlier in this article, approximately one-third of global fertiliser trade passes through the Strait of Hormuz under normal conditions. A prolonged blockade, therefore, creates a food security risk that operates on a slower timescale than the immediate energy price shock, but is potentially just as severe in its long-term consequences.

Fertiliser price spikes caused by supply disruptions translate into higher agricultural production costs within weeks. However, the full impact on food prices and crop yields takes longer to materialise — typically one to two growing seasons. This lag means that the food security consequences of a sustained Hormuz blockade could continue to unfold for months or even years after the waterway itself is reopened.

For developing nations that are both net energy importers and net food importers, this creates a particularly cruel compounding effect. They face higher fuel costs immediately. Then, several months later, they face higher food prices as the fertiliser supply disruption works its way through global agricultural supply chains. International humanitarian organisations have consistently flagged this sequential shock dynamic as one of the most underappreciated risks associated with sustained Hormuz disruptions.

Why the Effects Are Always Global — Not Just Regional

Perhaps the most important insight about Hormuz disruptions is that their consequences are never contained to the Middle East. The strait sits at the centre of a web of global supply chains so deeply interconnected that a shock at this single point radiates outward to affect fuel prices in European capitals, electricity supplies in Asian megacities, food costs in African markets, and industrial production schedules in North American factories.

This is the true meaning of the Strait of Hormuz’s strategic importance. It is not simply that the strait carries a lot of oil. It is that the global economy has been built, over decades, on the assumption that this oil will flow continuously and reliably. When that assumption is violated — even briefly, even partially — the resulting disruption exposes just how little redundancy exists in the world’s energy supply infrastructure, and how few realistic alternatives are available at the scale and speed that modern economies require.

A History of Threats to the Strait of Hormuz

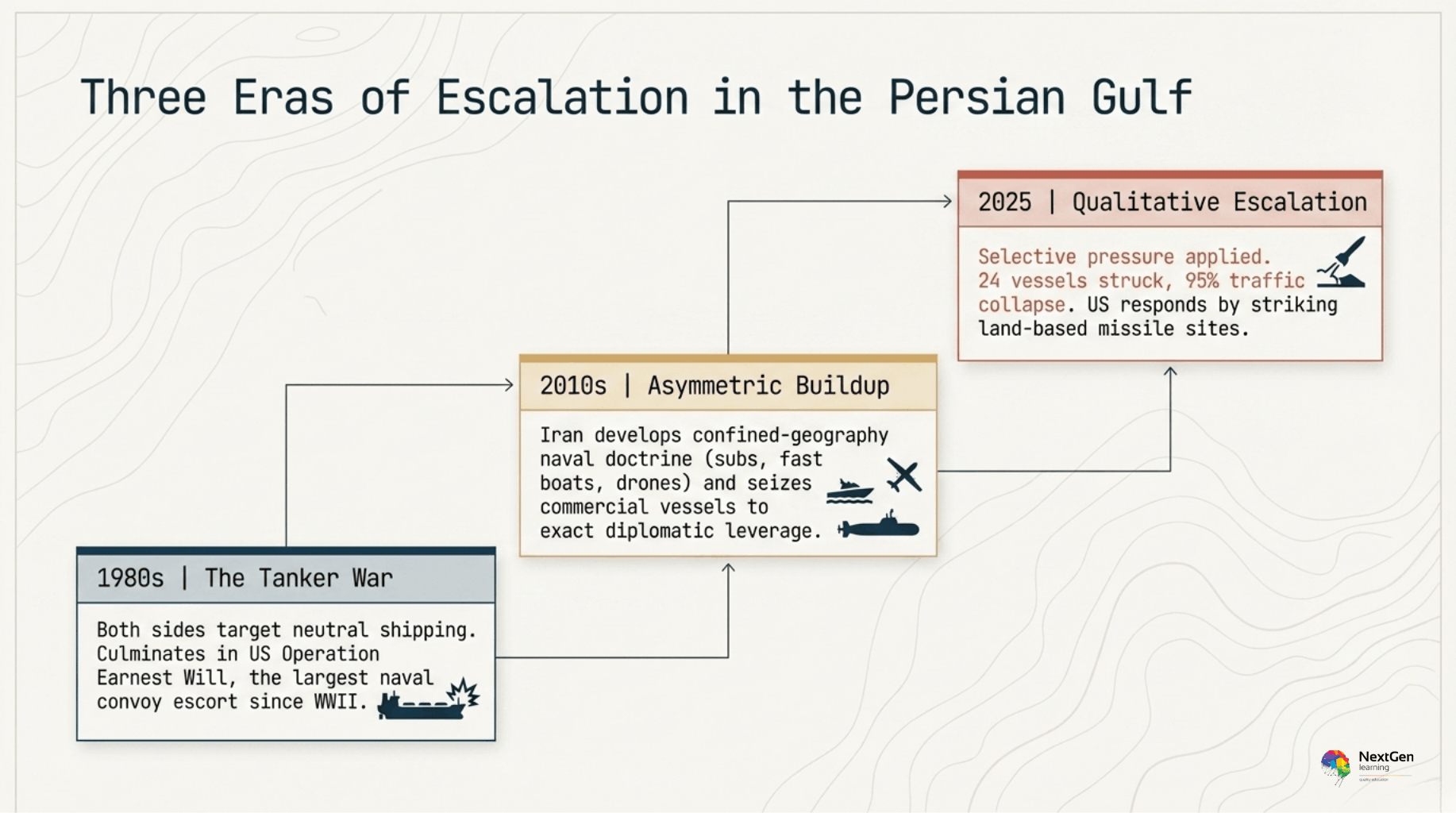

The 2025 Iran conflict did not emerge from nowhere. Iran’s willingness to threaten and disrupt traffic through the Strait of Hormuz is rooted in decades of strategic calculation, military development, and geopolitical confrontation. To understand the present, it is essential to understand the history, because the patterns that defined previous crises in the strait have shaped every aspect of how the current situation unfolded.

- 1980s — The Tanker War: Iran and Iraq attack neutral shipping; US launches Operation Earnest Will

- 2010s — Asymmetric Buildup: Iran develops confined-geography naval doctrine; seizes commercial vessels

- 2025 — Qualitative Escalation: 95% traffic collapse; 24 vessels struck; selective pressure applied by nationality

The Iran-Iraq Tanker War (1980s) — The First Modern Hormuz Crisis

The modern history of threats to the Strait of Hormuz begins with the Iran-Iraq War, which lasted from 1980 to 1988. This devastating eight-year conflict between two of the Gulf’s major oil producers gradually escalated from a land war into a full-scale assault on regional energy infrastructure — and ultimately into a direct threat to international shipping throughout the Persian Gulf.

By the mid-1980s, both Iran and Iraq had begun targeting oil tankers and commercial vessels belonging to neutral nations. The strategic logic was straightforward and brutal. Each side sought to deprive the other of oil export revenues while simultaneously pressuring the international community to intervene on their behalf. The result was what became known as the “Tanker War” — a sustained campaign of attacks on commercial shipping that made the Persian Gulf one of the world’s most dangerous maritime environments.

Iraq targeted tankers carrying Iranian oil, while Iran attacked ships serving Iraq’s Gulf Arab supporters — particularly Kuwait, which was financing Iraq’s war effort and allowing its ports to be used for Iraqi oil exports. Iranian Revolutionary Guard speedboats, shore-based missiles, and naval mines became the primary weapons of this maritime campaign. Dozens of vessels were damaged or sunk. Insurance premiums for Gulf shipping reached levels that threatened to make the entire trade economically unviable.

The crisis reached a turning point when Kuwait formally requested international protection for its tankers. The United States responded by launching Operation Earnest Will in 1987 — one of the largest naval convoy escort operations since the Second World War. American warships began escorting reflagged Kuwaiti tankers through the Gulf, providing direct military protection against Iranian attack. The Soviet Union also escorted some Kuwaiti vessels, making Hormuz a theatre of Cold War naval competition as well as regional conflict.

The operation was not without incident. In May 1987, an Iraqi aircraft — apparently by mistake — fired two Exocet missiles at the USS Stark, killing 37 American sailors. In April 1988, the US Navy engaged Iranian naval forces directly in Operation Praying Mantis — the largest American naval surface engagement since the Second World War — destroying two Iranian oil platforms, sinking several Iranian vessels, and significantly degrading Iran’s naval capacity in the Gulf.

The tanker war ultimately ended with the broader Iran-Iraq ceasefire in August 1988. However, it left enduring lessons. It demonstrated that Iran was willing to use the strait as a weapon of economic warfare. It showed that commercial shipping was acutely vulnerable to even relatively unsophisticated military threats in a confined waterway. And it established the precedent of American military intervention to protect freedom of navigation through the Gulf — a precedent that has shaped US strategic thinking about the region ever since.

Iranian Threats and Seizures — The 2010s and 2020s

Following the tanker war, the Strait of Hormuz entered a period of relative stability — though never complete calm. Iran periodically threatened to close the strait during diplomatic confrontations with the West, particularly as international sanctions over its nuclear programme intensified in the early 2010s. These threats were taken seriously by energy markets and defence planners, even when they did not result in actual military action.

In January 2012, as the European Union moved toward an embargo on Iranian oil imports, Iranian military officials issued explicit warnings that Iran would close the Strait of Hormuz if its oil exports were sanctioned. The threats caused immediate turbulence in global oil markets. The US Sixth Fleet issued counter-warnings that any attempt to close the strait would be regarded as an act of war. Ultimately, Iran did not follow through — but the episode demonstrated the enduring power of the strait as a lever of Iranian strategic pressure.

Throughout the mid-2010s, Iran developed and refined a doctrine of asymmetric naval warfare specifically designed for the confined geography of the Persian Gulf and the Strait of Hormuz. This doctrine — sometimes described as “swarming” — relies on large numbers of fast attack boats, shore-based anti-ship missiles, submarines, and naval mines to overwhelm or deter superior conventional naval forces. Rather than attempting to match the US Navy ship-for-ship, Iran invested heavily in capabilities specifically suited to denying access to the strait and threatening traffic within it.

The late 2010s saw this doctrine move from theory to practice. In a series of incidents between 2019 and 2021, Iranian forces seized or interfered with commercial vessels in the strait and surrounding waters. In June 2019, two oil tankers — the MT Front Altair and the MV Kokuka Courageous — were attacked near the Gulf of Oman in incidents the US attributed to Iran. In July 2019, Iran seized the British-flagged tanker Stena Impero, holding it and its crew for more than two months. In 2021, Iranian forces attempted to seize an Asphalt Princess tanker off the UAE coast.

Each of these incidents served a dual purpose. They demonstrated Iran’s capability and willingness to act against commercial shipping. They also sent a clear message to the international community that Iran retained the ability to make the strait dangerous whenever it chose to do so — without necessarily triggering a full military confrontation.

The 2025 Iran War Blockade — What Happened

The events of 2025 represented a qualitative escalation beyond anything seen in previous episodes of Hormuz tension. When the United States and Israel launched military strikes against Iran on 28 February 2025, Tehran responded by moving to effectively block the strait — not through a formal declaration of closure, but through a sustained campaign of military pressure that made commercial transit practically impossible for most operators.

Iranian drones, cruise missiles, fast attack boats, and potentially naval mines created conditions in which insuring vessels for transit became prohibitively expensive or simply unavailable. As a result, daily shipping traffic through the strait collapsed by approximately 95% compared to pre-conflict levels. The scale of this reduction was unprecedented. Even at the height of the 1980s tanker war, traffic through the Gulf was never reduced to this degree.

As of early April 2025, non-profit organisation United Against Nuclear Iran documented that at least 24 commercial vessels had been struck, with three additional near misses. The attacks were not indiscriminate — Iran appeared to apply selective pressure, allowing some vessels with connections to friendly nations to pass while targeting others. Between 1 and 15 March, eleven China-linked vessels transited the strait. On 3 April, a French container ship — reportedly the first Western vessel to pass through — crossed alongside three Oman-linked tankers and a Japanese gas carrier. On 31 March, Beijing expressed formal gratitude after three Chinese vessels, including two container ships belonging to state-owned shipping giant Cosco, passed safely through.

This selective approach was strategically sophisticated. By allowing Chinese and some other vessels to pass while targeting Western-linked shipping, Iran sought to drive a wedge between the US-led coalition and nations — particularly China — that had strong commercial incentives to maintain working relationships with Tehran. It was, in essence, an attempt to use the strait not just as a blunt instrument of economic disruption, but as a precision tool of geopolitical manipulation.

The US military response focused primarily on air strikes against Iranian military infrastructure rather than direct naval escort operations in the strait itself. On 18 March, the US military reported striking Iranian anti-ship cruise missile sites along the strait. However, the decision not to deploy American warships directly into the contested waterway reflected the genuine danger posed by Iran’s asymmetric naval capabilities in such a confined environment — and the risk of escalation that direct naval confrontation would have entailed.

President Trump called on US allies and China to contribute warships to help secure the strait. His request was met with limited enthusiasm. Most US allies were reluctant to commit naval forces to a confrontation with Iran without a clearer legal mandate and a more defined operational plan. China, despite its enormous economic stake in keeping the strait open, declined to participate in what it viewed as an American-led military operation against a country with which it maintained important strategic and commercial ties.

The ceasefire, when it came, was conditioned explicitly on Iran’s guarantee of safe passage through the strait. The immediate 15% drop in oil prices that followed the announcement was perhaps the clearest possible illustration of how much the global economy had been paying — in elevated energy costs, supply uncertainty, and disrupted trade — for every day that the strait remained effectively closed.

The Pattern Across Three Eras

Looking across these three distinct historical episodes — the 1980s tanker war, the 2010s pattern of seizures and threats, and the 2025 blockade — several consistent patterns emerge.

Iran has consistently demonstrated a willingness to use the Strait of Hormuz as a strategic instrument when it perceives itself to be under sufficient external pressure. The threshold for activation appears to be correlated with the severity of the threat Iran faces — economic sanctions alone have historically prompted threats but not action, while direct military strikes appear to cross the threshold into actual disruption.

Moreover, Iran’s capabilities in the strait have grown substantially with each passing decade. The fast attack boats and mines of the 1980s have been supplemented and in many respects superseded by sophisticated anti-ship missiles, armed drones, and submarine capabilities specifically designed for the confined geography of the Gulf. Each successive crisis has therefore been more difficult to manage militarily than the last — a trend that carries sobering implications for the future.

Finally, the international response to the Hormuz crisis has consistently struggled to keep pace with the speed and severity of Iranian action. The combination of legal ambiguity, alliance coordination challenges, and the genuine military risks of operating in a confined waterway against a prepared coastal defender has repeatedly constrained the options available to the US and its partners. Understanding this historical pattern is essential for evaluating the realistic prospects for long-term security in the strait.

Can Countries Bypass the Strait of Hormuz?

Every time tensions rise in the Strait of Hormuz, the same question surfaces in energy markets, government briefing rooms, and newspaper headlines: Can the world simply route its oil around the problem? The honest answer is that bypass options exist — but they are far too limited, too slow to scale, and too vulnerable to disruption to serve as a genuine alternative to the strait itself. Understanding precisely why requires a close look at what the existing infrastructure can and cannot do.

The Persistent Threat That Drove Bypass Development

The recurring threat of Hormuz closure has not gone unnoticed by the Gulf states most dependent on the waterway for their export revenues. Over several decades, Saudi Arabia and the UAE, in particular, have invested heavily in overland pipeline infrastructure specifically designed to allow some portion of their oil exports to bypass the strait entirely. These investments were deliberate and strategic — a direct response to the vulnerability exposed by the 1980s tanker war and reinforced by every subsequent episode of Hormuz tension.

However, building bypass infrastructure is extraordinarily expensive, technically demanding, and ultimately constrained by geography. Pipelines must traverse hundreds of kilometres of desert terrain. They require pumping stations, maintenance infrastructure, and secure terminal facilities at both ends. Furthermore, their capacity is fixed at the time of construction and cannot be rapidly scaled upward in response to an acute crisis. Consequently, while the bypass routes that exist today represent genuine engineering achievements, they were designed to provide partial redundancy — not to replace Hormuz entirely.

Saudi Arabia’s East-West Crude Oil Pipeline

The most significant bypass route currently in operation is Saudi Arabia’s East-West Crude Oil Pipeline, sometimes referred to as the Petroline. Stretching approximately 1,200 kilometres across the Arabian Peninsula, it connects Saudi Arabia’s eastern oil fields — located near the Gulf coast — to the Red Sea port of Yanbu on the country’s western coast. From Yanbu, tankers can load crude oil and transport it through the Red Sea, the Suez Canal, and onward to European and other global markets without ever passing through the Strait of Hormuz.

The East-West Pipeline has a maximum capacity of approximately five million barrels of crude oil per day, according to US government data. Under normal operating conditions, it typically runs at well below this maximum, since most Saudi oil exports travel eastward through Hormuz toward Asian markets — the destination for the majority of Gulf crude. However, in a crisis scenario, Saudi Arabia could theoretically redirect a significant portion of its production through the pipeline and away from Hormuz.

In the past, Saudi Arabia has also demonstrated creative flexibility with its pipeline infrastructure. On at least one occasion, it temporarily repurposed a natural gas pipeline to carry crude oil — a pragmatic workaround that expanded effective bypass capacity beyond what the dedicated oil pipeline alone could provide. This kind of operational improvisation is valuable, but it has limits. Repurposed pipelines are not optimised for crude oil transport, and the conversion process takes time — time that may not be available during an acute supply crisis.

Furthermore, the East-West Pipeline’s Red Sea terminus at Yanbu is not entirely free from geopolitical risk. The Red Sea itself has experienced significant security challenges in recent years, most notably from Houthi missile and drone attacks on commercial shipping that began in late 2023 and continued into 2025. Consequently, routing oil through the East-West Pipeline does not simply exchange one risk for zero risk — it exchanges one set of risks for a different, though generally lower, set of risks.

The UAE’s Habshan-Fujairah Pipeline

The United Arab Emirates has developed its own bypass infrastructure in the form of the Habshan-Fujairah Pipeline, which connects the UAE’s inland oilfields in Abu Dhabi to the port of Fujairah on the Gulf of Oman coast. Fujairah sits outside the Strait of Hormuz — on its eastern, seaward side — which means that oil loaded at Fujairah can reach the Arabian Sea and global shipping routes without transiting the strait at all.

The Habshan-Fujairah Pipeline has a daily capacity of at least 1.5 million barrels. For the UAE, this represents a meaningful degree of energy export resilience. In a scenario where Hormuz is partially or fully blocked, the UAE can continue exporting a significant volume of oil through Fujairah while other Gulf producers are more severely constrained.

However, the 2025 conflict exposed an important vulnerability in this apparently secure bypass route. Oil loading operations at Fujairah were disrupted by drone attacks during the conflict — a reminder that even facilities outside the strait itself are not necessarily safe from Iranian military reach. Iran’s growing drone and missile capabilities mean that the geographical advantage of Fujairah’s position outside the strait no longer guarantees immunity from attack. Consequently, the Habshan-Fujairah Pipeline provides genuine bypass capacity under normal or moderately elevated threat conditions, but its reliability degrades significantly when Iran is willing to conduct offensive operations at extended range.

Why Bypass Routes Are Not a Complete Solution

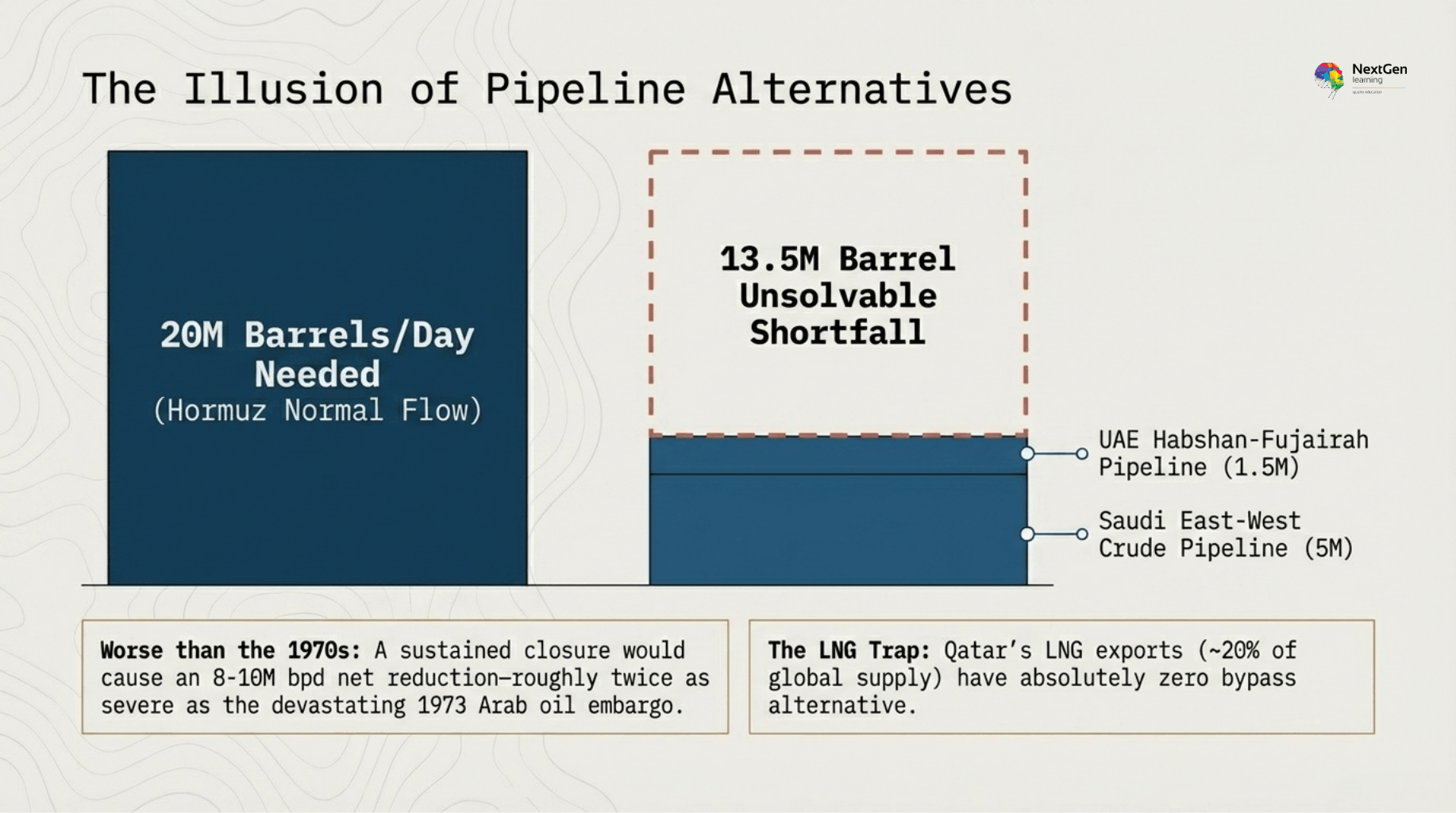

Even if both the Saudi East-West Pipeline and the UAE Habshan-Fujairah Pipeline were operating simultaneously at maximum capacity — and even if both were completely free from any threat of attack — the combined bypass capacity would still fall dramatically short of replacing Hormuz. The arithmetic is unforgiving.

- Saudi Arabia: Up to 5 million barrels per day via East-West Pipeline to Yanbu

- UAE: Up to 1.5 million barrels per day via Habshan-Fujairah Pipeline

- Iraq: Zero bypass capacity — entirely dependent on Hormuz

- Kuwait: Zero bypass capacity — entirely dependent on Hormuz

- Qatar LNG: Zero bypass alternative — no pipeline option exists at the required scale

Under normal conditions, approximately 20 million barrels of oil and oil products transit the Strait of Hormuz every day. The maximum combined capacity of the two major bypass pipelines — Saudi Arabia’s five million barrels per day and the UAE’s 1.5 million barrels per day — amounts to approximately 6.5 million barrels per day. That leaves a shortfall of roughly 13.5 million barrels per day that has no bypass alternative whatsoever.

Reuters reporting during the 2025 conflict estimated that diverting oil to bypass infrastructure would lead to a net supply reduction of between 8 and 10 million barrels per day — even accounting for some additional improvised routing measures. To place that figure in context, the largest single supply shock in the history of global oil markets — the Arab oil embargo of 1973 — involved a reduction of approximately 4 to 5 million barrels per day. A sustained Hormuz closure with bypass routes operating at full capacity would therefore represent a supply shock roughly twice as severe as the most disruptive energy crisis of the 20th century.

The other Gulf producers — Iraq, Kuwait, Qatar, and Bahrain — have essentially no meaningful bypass capacity at all. Iraq, which exports approximately 3.3 million barrels per day and depends on those revenues for the vast majority of its government budget, has no pipeline route to a non-Hormuz port. Kuwait is similarly constrained. Qatar’s LNG exports — which represent approximately 20% of global LNG supply — have no bypass alternative; LNG cannot be transported by pipeline over the distances involved, and there is no LNG export terminal outside the Gulf accessible to Qatari producers.

The Infrastructure Gap — A Long-Term Vulnerability

The fundamental problem is not simply that current bypass capacity is inadequate. It is that building sufficient bypass capacity to genuinely replace Hormuz would require an investment so large and so geographically challenging that it has never been seriously attempted — and realistically, never will be.

Constructing enough pipeline infrastructure to move 20 million barrels per day across the Arabian Peninsula would require dozens of parallel pipeline systems, hundreds of pumping stations, and multiple new deep-water port terminals. The cost would run into hundreds of billions of dollars. The construction timeline would stretch over decades. And the resulting infrastructure would still be vulnerable to military attack — as Fujairah demonstrated during the 2025 conflict.

Moreover, LNG cannot be transported by pipeline over the distances involved in any realistic bypass scenario. Qatar’s LNG exports have no overland alternative route. If the strait closes, Qatari LNG simply does not reach global markets — there is no workaround. This reality makes the bypass problem for gas supply even more intractable than for oil.

Strategic Petroleum Reserves — The Short-Term Buffer

The closest thing the world has to a genuine short-term bypass for Hormuz disruptions is not infrastructure — it is inventory. The International Energy Agency coordinates a collective strategic petroleum reserve system among its member nations, which are required to maintain reserves equivalent to at least 90 days of net oil imports. In an acute supply emergency, member nations can collectively release these reserves into global markets to cushion the price impact and buy time for diplomatic or military resolution of the underlying crisis.

The IEA coordinated strategic reserve releases during several previous supply emergencies, including after Hurricane Katrina in 2005 and during the Libyan civil war in 2011. However, strategic reserves are a finite buffer — not a long-term solution. They are designed to manage short, sharp supply shocks, not sustained disruptions lasting months or years. A prolonged Hormuz closure would exhaust collective strategic reserves within weeks to months, leaving markets fully exposed to the underlying supply shortfall.

Furthermore, strategic reserves are held primarily by IEA member nations, which are predominantly wealthy, developed economies. Many of the countries most severely affected by Hormuz disruptions, particularly in Asia and Africa, have limited strategic reserve capacity and would therefore be exposed to the full force of price increases much sooner than wealthier nations with larger buffers.

The Honest Assessment

The honest assessment of bypass capacity is therefore this: the infrastructure that exists today can reduce the severity of a Hormuz disruption at the margins. It cannot prevent a global supply crisis if the strait is closed for an extended period. Saudi Arabia and the UAE have made meaningful investments in resilience, and those investments provide real value. However, they were never designed — and are not capable — of replacing the Strait of Hormuz as the primary export route for Gulf energy.

This reality has profound implications for global energy security policy. It means that keeping Hormuz open is not simply one option among several. It is, for the foreseeable future, a non-negotiable requirement of global economic stability. Every barrel of oil that the world consumes, every kilowatt of electricity generated from Gulf gas, and every tonne of food grown with Middle Eastern fertiliser depend, ultimately, on the continued free flow of traffic through a corridor 33 kilometres wide — and on the fragile combination of diplomacy, deterrence, and military power that keeps it open.

The Strait of Hormuz and Global Energy Security — What Comes Next?

The 2025 Iran conflict and its near-paralysis of the Strait of Hormuz did not create the world’s energy security problem. It revealed it. The vulnerability had always been there — embedded in decades of globalised energy trade built around the assumption that this single narrow waterway would remain perpetually open. What the crisis did was force governments, energy companies, and strategic planners to confront, with uncomfortable directness, just how fragile that assumption truly is. The question now is what, if anything, can realistically be done about it.

The Long-Term Vulnerability of Global Oil Supply

The structural vulnerability of the global energy system to Hormuz disruption is not diminishing. In several important respects, it is growing. Global demand for Gulf oil and LNG has increased steadily over the past three decades, driven primarily by Asia’s extraordinary economic expansion. China, India, and the broader Asian emerging market bloc have collectively added hundreds of millions of energy consumers to the global demand pool. The overwhelming majority of the additional supply required to meet that demand has come from Gulf producers — and the overwhelming majority of that supply flows through Hormuz.

At the same time, Iran’s military capabilities specifically relevant to the strait have grown considerably. The drone and missile technologies that Iran deployed during the 2025 conflict are substantially more sophisticated than the speedboats and mines that defined the 1980s tanker war. Furthermore, Iran has invested heavily in the mass production of relatively low-cost armed drones — a technology that has proven highly effective at threatening commercial shipping while being difficult and expensive to defend against at scale. Consequently, the cost and complexity of guaranteeing safe passage through Hormuz against a determined Iranian threat has increased substantially, even as the importance of that passage to the global economy has grown.

The geopolitical environment surrounding the strait has also become more complex. The emergence of a closer strategic alignment between Iran, Russia, and China — sometimes described as an axis of convenience rather than a formal alliance — creates a situation in which Western-led efforts to enforce freedom of navigation in the strait face not just Iranian resistance, but the broader geopolitical complications of confronting a loosely coordinated bloc of major powers. Russia has strong incentives to support Iranian leverage over Hormuz, since higher oil prices benefit Russian energy revenues. China, despite its enormous economic stake in keeping the strait open, is reluctant to align openly with US-led enforcement operations that it views as part of a broader American strategy of containment.

Could the World Reduce Its Dependence on Hormuz?

The most fundamental long-term solution to the Hormuz vulnerability problem is not military — it is structural. If the world consumed less Gulf oil and LNG, the strategic leverage that Hormuz provides to Iran would diminish proportionally. In theory, three pathways could reduce global dependence on the strait over the long term.

The first pathway is energy transition. As renewable energy sources — solar, wind, and battery storage — continue to expand their share of global electricity generation, the demand for fossil fuels in the power sector should gradually decline. Electric vehicles, moreover, reduce demand for oil in the transport sector. If the energy transition proceeds at the pace envisioned by the International Energy Agency’s net-zero scenarios, global oil demand could peak within this decade and begin a sustained structural decline. Under those circumstances, the relative importance of Gulf oil — and therefore of Hormuz — would gradually diminish over the coming decades.

However, the energy transition is proceeding unevenly. Wealthy nations are decarbonising their power sectors at meaningful speed. However, developing economies — precisely the ones most dependent on affordable fossil fuel imports — are expanding their energy consumption faster than they are deploying renewables. For many Asian and African nations, coal and oil remain the most economically accessible energy sources in the near term. Consequently, while the energy transition will eventually reduce global Hormuz dependence, that reduction is likely to be gradual, uneven, and far slower than the pace required to address the vulnerability within the current strategic timeframe.

The second pathway is supply diversification. Importing nations can reduce their exposure to Hormuz by sourcing a greater proportion of their energy from non-Gulf producers. The United States, for instance, has substantially reduced its own dependence on Gulf oil through the shale revolution — American domestic production now covers a much larger share of US demand than it did a decade ago. American LNG exports have also provided some European nations with an alternative to Russian pipeline gas, and could in principle provide some Asian markets with an alternative to Qatari LNG.

However, supply diversification has its limits. The Gulf region contains the world’s largest and most cost-effective oil reserves. Non-Gulf producers — whether in North America, Brazil, West Africa, or elsewhere — generally have higher production costs and more limited reserve bases. Therefore, while diversification can reduce marginal dependence on Gulf oil at the edges, it cannot realistically replace the volume and cost-competitiveness of Gulf production for the world’s largest energy consumers. Moreover, American LNG capacity, while growing, remains insufficient to replace Qatari LNG for Asia’s largest importers in anything approaching the near term.

The third pathway is demand reduction through energy efficiency. More fuel-efficient vehicles, better-insulated buildings, more efficient industrial processes, and smarter urban planning can all reduce the total volume of energy that economies need to function. Improvements in energy efficiency reduce import dependence without requiring either a switch to different energy sources or a fundamental restructuring of supply chains. Furthermore, efficiency improvements tend to be economically beneficial in their own right — they reduce costs for businesses and consumers regardless of their geopolitical implications.

In practice, all three pathways will need to be pursued simultaneously and over an extended timeframe. None of them offers a near-term solution to the vulnerability that the 2025 crisis exposed so vividly. For at least the next decade — and quite possibly longer — the world will remain profoundly dependent on the free flow of energy through the Strait of Hormuz.

The Role of Strategic Petroleum Reserves — Reform and Expansion

The 2025 crisis exposed significant weaknesses in the global strategic petroleum reserve system. As discussed earlier, collective IEA reserves are designed to manage short, sharp supply shocks — not sustained disruptions. Furthermore, many of the nations most acutely affected by Hormuz disruptions, particularly in Asia and Africa, are not IEA members and therefore do not participate in the coordinated reserve release mechanism.

Several reform proposals have gained traction in the aftermath of the crisis. One is the expansion of IEA membership to include major Asian energy consumers — most importantly China and India — in a formalised reserve coordination framework. Bringing these nations into the collective reserve system would both expand the total volume of reserves available for emergency release and ensure that coordinated responses to supply emergencies are genuinely global rather than primarily Western in their coverage.

A second proposal is the expansion of strategic reserve capacity in Asian nations that currently hold relatively modest inventories. Japan and South Korea have well-developed reserve systems. However, China, India, and many Southeast Asian nations hold reserves that, while growing, fall short of the 90-day standard maintained by IEA members. Expanding Asian reserve capacity would provide a more substantial buffer against future Hormuz disruptions and reduce the speed at which supply shocks translate into domestic fuel shortages and price spikes.

A third area of reform involves the diversification of reserve storage locations. Holding strategic reserves in geographically dispersed facilities — including some outside the home nation — reduces the vulnerability of reserve stocks to the same geopolitical disruptions that triggered their need in the first place.

Naval and Diplomatic Frameworks for Long-Term Security

Beyond energy policy, the 2025 crisis has reinvigorated debate about the international frameworks needed to secure freedom of navigation through the Strait of Hormuz on a sustainable long-term basis.

The US-led approach of bilateral deterrence — maintaining sufficient naval presence in the region to make Iranian closure attempts prohibitively costly — has been the dominant strategy for decades. However, the 2025 conflict exposed its limitations. The cost and risk of deploying American naval forces into a confined waterway against Iran’s asymmetric capabilities are substantial. Furthermore, the political willingness of US administrations to sustain that commitment varies with domestic political priorities and the availability of military resources for other theatres.

A more durable framework would involve broader multilateral participation in Hormuz security. The nations with the greatest economic stake in keeping the strait open — China, Japan, South Korea, India, and the major European economies — all have powerful incentives to contribute to its security. However, translating those incentives into coordinated military commitments has proven extremely difficult, primarily because of the geopolitical complications involved in aligning nations with very different relationships with Iran and with each other.

Some analysts have proposed a formal international maritime security framework for the Strait of Hormuz — analogous in some respects to the international naval coalitions that have operated in the Red Sea and the Gulf of Aden. Such a framework would distribute the burden of security provision more broadly, reduce dependence on US unilateral commitment, and provide a clearer legal mandate for protective operations. However, achieving the necessary international consensus for such a framework — particularly given China’s ambivalence and Russia’s active opposition — remains a formidable diplomatic challenge.

Diplomatic engagement with Iran itself remains, ultimately, the most sustainable path to long-term Hormuz security. A negotiated framework that addresses Iran’s core security concerns — sanctions relief, recognition of its regional interests, and credible guarantees against military attack — while securing meaningful commitments to freedom of navigation would represent the most durable possible resolution. The 2025 ceasefire, conditioned on Iran’s guarantee of safe passage, represents a fragile first step in that direction. However, the deeper structural tensions that produced the crisis — Iran’s nuclear programme, its support for regional proxy forces, and its fundamental hostility to the US-led regional order — remain unresolved.

The Uncomfortable Conclusion

The uncomfortable conclusion that emerges from a clear-eyed assessment of the Strait of Hormuz’s future is this: the world has no good options for eliminating its dependence on this waterway within any politically or economically realistic timeframe. The energy transition offers a long-term structural solution, but its timeline extends over decades. Supply diversification can reduce vulnerability at the margins but cannot replace Gulf volumes. Bypass infrastructure is genuinely inadequate. Strategic reserves provide a short-term buffer but not a long-term solution. And diplomatic resolution of the underlying tensions with Iran, while essential, remains elusive.

What the world can do — and what the 2025 crisis should motivate it to do with far greater urgency — is invest more seriously in all of these partial solutions simultaneously. Every additional million barrels of non-Gulf production capacity, every additional day of strategic reserve coverage, every additional gigawatt of renewable energy generation, and every additional kilometre of bypass pipeline capacity reduces, at least marginally, the leverage that this 33-kilometre waterway holds over the global economy.

Moreover, the crisis should serve as a powerful reminder of the true cost of energy security — not just in financial terms, but in terms of geopolitical risk, human welfare, and the fragility of the interconnected systems on which modern civilisation depends. The Strait of Hormuz will remain the world’s most important oil chokepoint for the foreseeable future. Keeping it open is not a foreign policy preference. It is an economic necessity — and managing that necessity wisely is one of the defining strategic challenges of the coming decades.

Frequently Asked Questions About the Strait of Hormuz

The Strait of Hormuz is the world’s single most critical oil chokepoint — a narrow maritime corridor through which approximately 20% of global oil supply and 20% of global liquefied natural gas passes every day. No other waterway on Earth handles a comparable volume of energy trade, and no realistic bypass alternative exists at sufficient scale to replace it.